Recent polling data reveals that 67% of Americans are expecting a housing market crash within the next three years. With all the media coverage recently, it’s understandable why many feel this way. Fortunately, current market indicators show that the situation today is far different than before 2008’s housing crash.

Back Then, Mortgage Standards Were Less Strict

Prior to the onset of the housing crisis, banks were engaging in a practice that facilitated easier access to home loans and refinancing. This policy enabled them to inflate the demand for housing, often at the expense of sound lending criteria. As a result, it was relatively straightforward for nearly any individual to qualify for a home loan or refinance an existing one.

Banks and other lending institutions assumed a great deal more risk when they changed their lending criteria, both in terms of the borrower and the mortgage product offered. The result was high levels of defaults, foreclosures, and falling prices throughout the market. Now the situation has been reversed – purchasers are held to much higher standards when it comes to obtaining a loan. Mortgage companies have tightened their requirements accordingly.

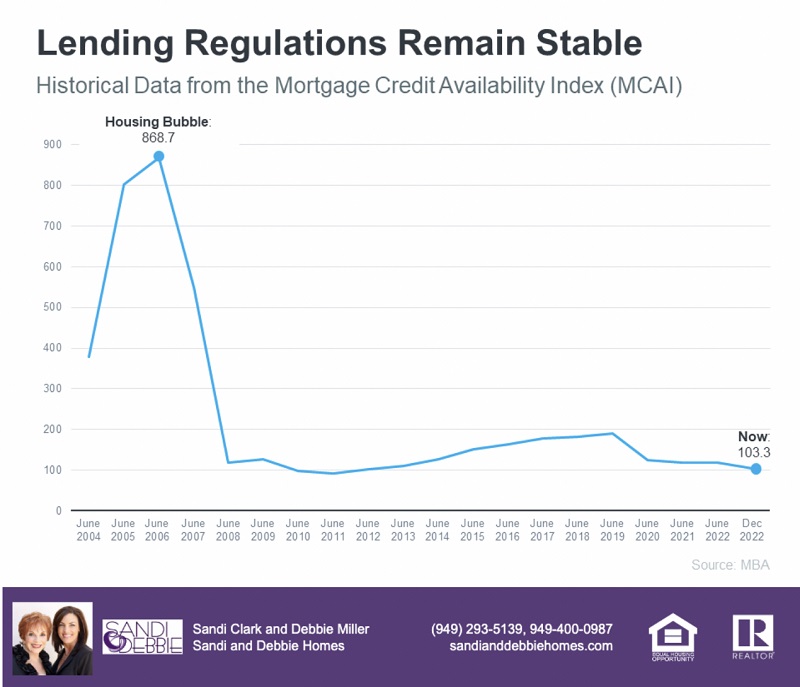

This graph from the Mortgage Bankers Association (MBA) provides an important informational snapshot. The index measures the ease or difficulty of obtaining a mortgage, with a higher number representing easier access and a lower number signifying greater difficulty. As demonstrated, this index can provide powerful insights into economic trends.

The data depicted in this graph is highly indicative of the difference in lending regulations between today and the period leading up to the market crash. Significantly stricter standards have been implemented, which have helped prevent a scenario where foreclosures reach levels comparable with pre-crash years.

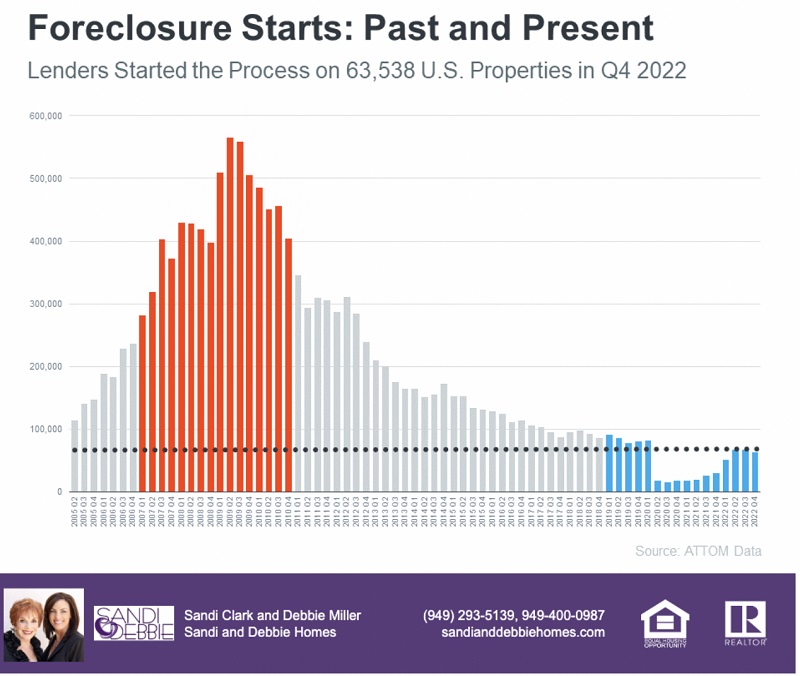

Foreclosure Volume Has Declined a Lot Since the Crash

The housing market has changed significantly since the bubble burst. Research from ATTOM indicates that fewer homeowners are facing foreclosure compared to before the crash due to more stringent qualification requirements for buyers, resulting in a lower likelihood of default. A comparison of pre-crash and current foreclosure activity is illustrated in the graph below:

The total number of foreclosures is low, and experts anticipate that it won’t skyrocket as it did in 2008. Bill McBride, the founder of Calculated Risk, has commented on the effects of home price increases following the Great Recession and why we should not expect something similar this time.

The bottom line is there will be an increase in foreclosures over the next year (from record level lows), but there will not be a huge wave of distressed sales as happened following the housing bubble. The distressed sales during the housing bust led to cascading price declines, and that will not happen this time.

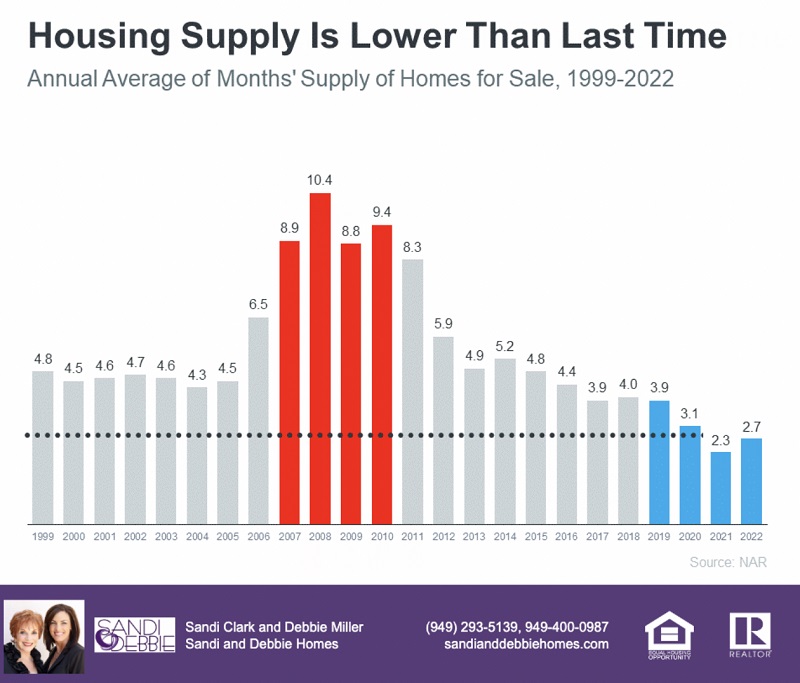

The Supply of Homes for Sale Today Is More Limited

In the past, during the housing crisis, there was an influx of homes on the market that led to a decrease in prices. Despite the fact that there has been an increase in supply this year, inventory levels are still low due to years of not building enough homes.

The National Association of Realtors (NAR) released data that shows today’s supply-and-demand ratio is significantly lower than the last time. The graph below illustrates how the current unsold inventory level hovers around 2.7 months’ supply at the present sales rate, making it less likely for prices to experience a dip similar to what occurred in the past. In other words, although some areas may see slight shifts in pricing indications, large drops in home prices are unlikely to occur.

What We Say…

If recent headlines have you worried we’re headed for another housing crash, the data above should help ease those fears. Expert insights and the most current data clearly show that today’s market is nothing like it was last time.

Leave a Reply